Is there national security without economic security?

The collapse of the China spy trial shows the cost of failing to protect our economic security by getting domestic investors to support our growth.

The collapse of the China spy case says more about Britain than China, and more about our economy than any Treasury forecast. The Government has made clear they think we have no choice: Beijing’s cash is more important than our laws.

That’s a generational failure based on decades of failing to understand risk, and it starts with the economy.

The UK’s insurance and pension funds hold more than £6 trillion in investable wealth. That’s huge and more than double our national debt, enough to put energy behind the ideas that will change the world - and make us rich. But the money isn’t in the minds of our entrepreneurs, instead it is stored in bonds. This is the illusion of prudence.

Our regulators have congratulated themselves in presiding over a generation of stagnation by following a model that prizes the management of risk over the pursuit of growth, we have confused volatility with danger and safety with success.

Like a farmer leaving his seeds in dry storage rather than planting them, we have built a system that minimises short-term shocks at the cost of long-term vitality. Our money is no longer alive in the economy. It sits idle as dead capital in a country that desperately needs movement.

Business, of course, won’t wait. If they can’t get the money they need to invest and employ from our own savings, they will look abroad making us dependent on the kindness of strangers until those foreigners have power over us.

The government’s evident fear of annoying Beijing shows we have reached the point where Whitehall believes Britain cannot sustain its own economy or defend its own interests without outside help. That is not strategy, it’s surrender.

What we call “de-risking” has turned into a form of self-denial, in which the fear of loss outweighs the hope of gain.

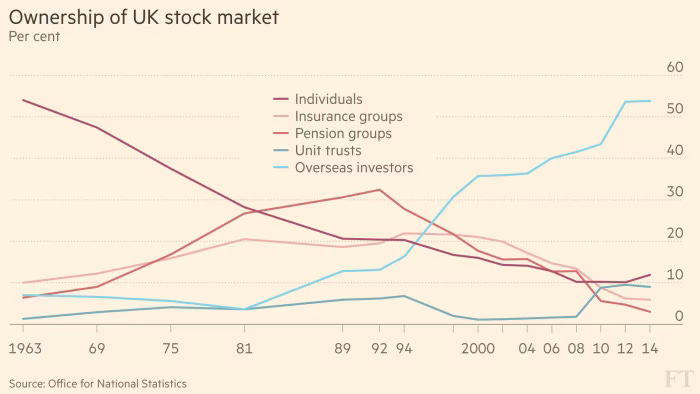

The results are visible everywhere. Business investment languishes near the bottom of the G7. Infrastructure projects stall for lack of financing. Promising companies sell to foreign buyers because they cannot raise funds at home. In the 1980s, British pension and insurance funds owned more than half of the London market; today they hold barely 4 per cent. The rest belongs mostly to foreign investors.

We have spent forty years withdrawing our own capital from our own country, and we are surprised to find our economy static and our Treasury dependent.

That distorts our politics. When a government cannot name a threat because it fears unsettling its creditors, we are no longer sovereign in any meaningful sense. The decision to block the prosecution was not a matter of legal detail; it was an act of economic self-censorship. We have reached a point where the flow of money dictates the bounds of our diplomacy. That is the measure of our decline.

The failure of our foreign policy, our defence, but most of all our economic planning, has been immense, still, there is a way out, but only if we are honest about the nature of the problem: Britain doesn’t lacks capital, we have forgotten how to use it.

We need to rediscover the distinction between live and dead money. Live money circulates through the economy - funding innovation, building infrastructure, creating value that compounds over generations. Dead money lies dormant, safe on a spreadsheet in bonds or buildings, slowly eroded by inflation and inertia.

We need to reverse the regulation and attitude that have clogged up the arteries of our economy for too long and design a financial system that rewards productive investment and doesn’t just punish volatility. It starts with what we save.

In Britain, most wealth is held in pensions and insurance funds where incentives and regulation have left pools of capital too small to take risk. Consolidating smaller schemes into larger, professional funds would allow them to take risk at scale allowing investment in the technologies, energy systems and industries that underpin national resilience.

But rules alone will not change culture. We need to recover the confidence to take risk and the understanding that the only way to secure prosperity is to invest in ourselves. Attracting foreign investment is no substitute for domestic commitment. All foreign capital is, by its nature, extractive. The question is whether the return to us is worth the price we pay for through extraction. If we can’t grow faster than the cost, then we’re just paying to have the bath filled while the plug is out.

The government needs to make Britain investable again, not only to others but to ourselves. Clear planning rules, stable regulation, and genuine long-term industrial priorities would give our own capital a reason to stay home; and releasing funds from the constraints of small holdings and the need to avoid volatility would allow British money backs British projects, making foreign investment a complement, not a crutch.

The lesson of the spy scandal has really about one thing: sovereignty. The government’s trepidation is not just political cowardice, or an intelligence failure, but a demonstration that our government does not believe in our future. While people across this country are working hard to make Britain strong and prosperous, Whitehall believes Britain depends on the economic permission from others. That’s the country we have to change, we have the capital, now we need to bring it back to life.

Short termism is the rule of the day 🇬🇧🇬🇧

You really should be shouting from the rooftops. The UK now is just a fire sale & our children & grandchildren will be inheriting nothing!